The narrative around real-world asset tokenization has shifted. Two years ago, every blockchain conference featured a “tokenization is coming” panel. In March 2026, tokenized RWAs excluding stablecoins crossed $25 billion in on-chain value nearly quadrupling from $6.4 billion a year earlier. Six distinct asset classes each exceed $1 billion on-chain. BlackRock’s BUIDL fund holds $1.9 billion. Ondo Finance manages $2.5 billion in tokenized treasury products.

This is not “coming.” This is infrastructure being built, deployed, and operated in production.

Simultaneously, the gap between the headline numbers and the engineering reality is wide. Most industry coverage focuses on market growth and institutional names. What rarely gets discussed is the infrastructure stack behind those numbers – the smart contracts, compliance middleware, settlement mechanics, and operational systems that make tokenized asset actually function as a financial product. That is what this article covers.

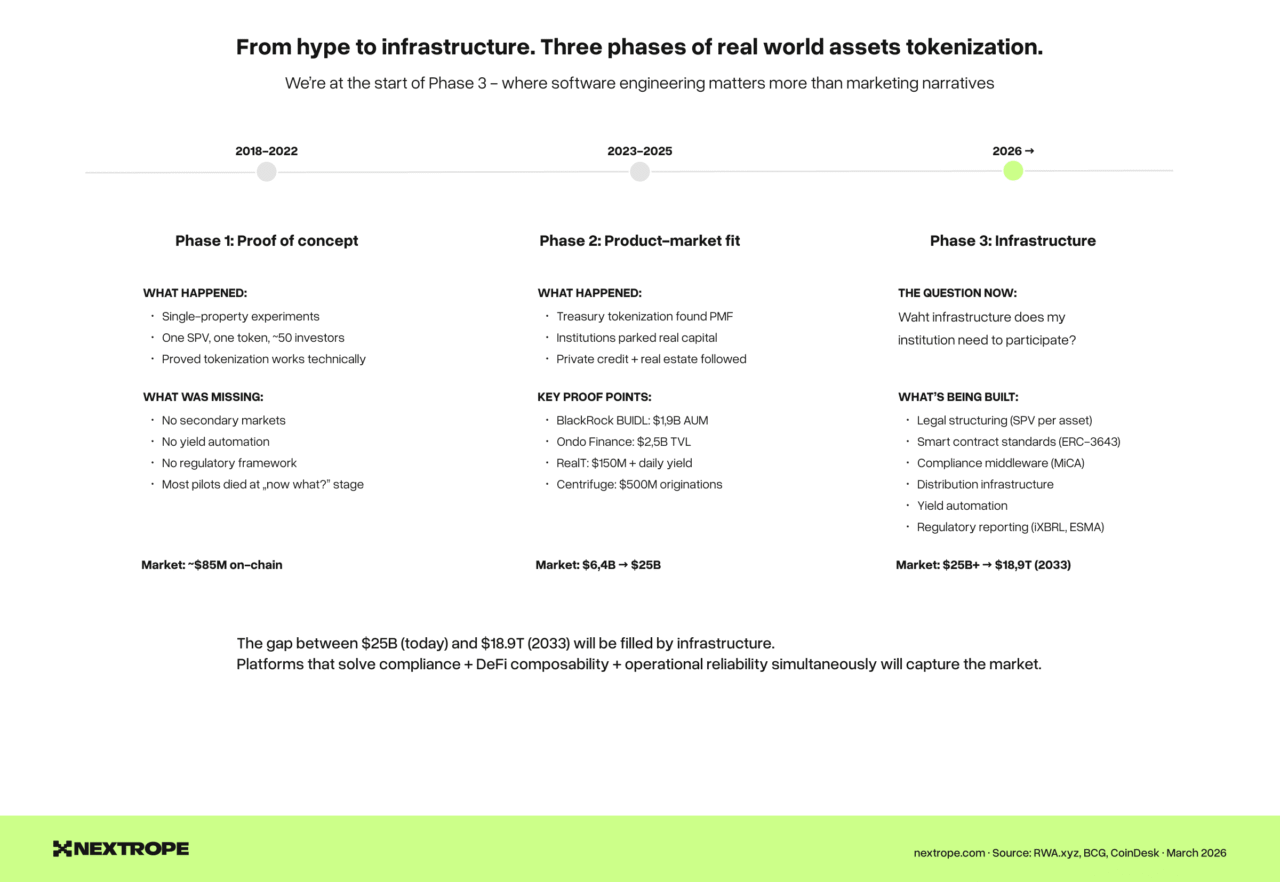

The three phases of real-world assets tokenization

Understanding where we are requires understanding where we came from.

Phase 1: Proof of concept (2018-2022). Single-property experiments. One SPV, one token, one blockchain, 50 investors. Proved that tokenization works technically. Did not prove it works operationally. Most pilots died at the “now what?” stage – tokens existed but had no secondary market, no yield distribution automation, and no regulatory framework.

Phase 2: Product-market fit (2023-2025). Treasury tokenization found product-market fit. BlackRock, Franklin Templeton, Ondo Finance proved that institutions will park capital in tokenized instruments when the yield is real and the custodial structure is institutional-grade. Private credit followed. Centrifuge crossed $500M in originations. RealT tokenized $150M in rental properties with automated daily yield.

Phase 3: Infrastructure buildout (2026-present). We are here now. The question is no longer “does tokenization work?” but “what infrastructure does my institution need to participate?” This is the phase where software engineering matters more than marketing narratives.

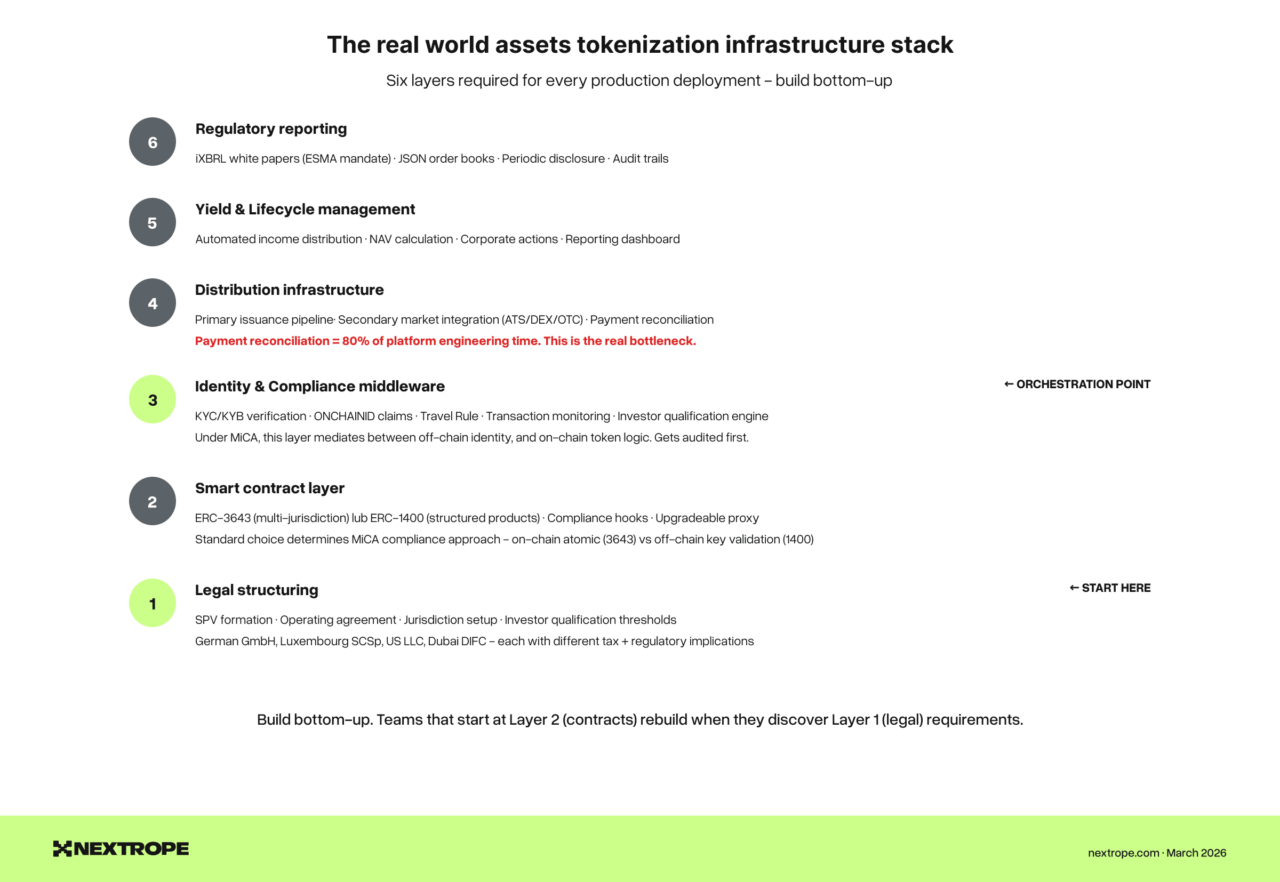

What infrastructure actually means?

When we say RWA tokenization has moved to infrastructure, we mean the following components are now necessary for any production deployment:

Legal structuring – SPV formation, operating agreements, jurisdiction-specific compliance. A token without a proper legal wrapper is a technical achievement with no commercial value. Dubai’s XRPL pilot demonstrates the pattern: title deed tokens backed by official land registry integration, with Asset-Referenced Virtual Assets (ARVAs) regulating trade conditions.

Smart contract layer – token standard selection (ERC-3643 for multi-jurisdiction compliance, ERC-1400 for structured products with partitions), compliance hooks, upgradeability, and transfer restriction logic. The standard choice has operational consequences. ERC-3643 enforces compliance on-chain atomically – the compliance check and the transfer happen in the same transaction. ERC-1400 validates off-chain, creating a timing gap that MiCA regulators will question. Our ERC-3643 vs ERC-1400 comparison maps this decision in detail.

Identity and compliance middleware – KYC/KYB verification, on-chain claim registry (ONCHAINID for ERC-3643), investor qualification engine, Travel Rule compliance, transaction monitoring. Under MiCA, this layer orchestrates the entire system. It mediates between off-chain identity and on-chain token logic. Our MiCA compliance checklist maps the engineering requirements.

Distribution infrastructure – primary issuance pipeline (investor onboarding → qualification → subscription → payment reconciliation → minting) and secondary market integration. The bottleneck is payment reconciliation – matching off-chain bank transfers to on-chain token allocations. This is where 80% of platform engineering time goes.

Yield and lifecycle management – automated income distribution, NAV calculation, corporate actions (dividends, splits, redemptions), and reporting. RealT’s daily stablecoin dividends via smart contracts set the standard. Any platform that distributes yield manually via spreadsheets will not scale.

Regulatory reporting – iXBRL white paper generation (ESMA mandate since December 2025), order book record-keeping in ESMA JSON format, periodic disclosure automation. Built last by most teams, asked about first by regulators.

The numbers behind the infrastructure

The market data tells a specific story about which infrastructure is being built and where:

Tokenized US treasuries (~$8.7B) are the largest category because they have the simplest infrastructure requirements. The underlying asset is fungible, the NAV updates daily, and the legal structure is well-established. BlackRock’s BUIDL and Ondo’s USDY/OUSG prove that institutional-grade Treasury tokenization works. The engineering challenge is not the smart contract – it is the integration with fund administrators, transfer agents, and banking rails.

Private credit (~$4B+) is the fastest-growing category requiring complex infrastructure. Each position has unique risk characteristics – different borrowers, terms, collateral, and maturity dates. ERC-1400 partitions handle multi-tranche waterfall distributions natively. Centrifuge and Maple Finance lead in infrastructure for this asset class.

Real estate (~$1.5B+) is the most legally complex. Every property requires an SPV. Compliance varies by municipality, not just country. Yield distribution depends on property management integration. Our real estate tokenization analysis covers the five patterns that separate successful projects from failed pilots.

Commodities (~$2B+, fastest growing) require proof-of-reserves systems linking on-chain supply to audited vault holdings. Gold dominates with Pax Gold and Tether Gold.

The total: $25 billion on-chain, up 245× since 2020. BCG and Ripple project $18.9 trillion by 2033. McKinsey estimates $2 trillion by 2030. The gap between current state and these projections will be filled by infrastructure – specifically, by platforms that solve regulatory compliance, DeFi composability, and operational reliability simultaneously.

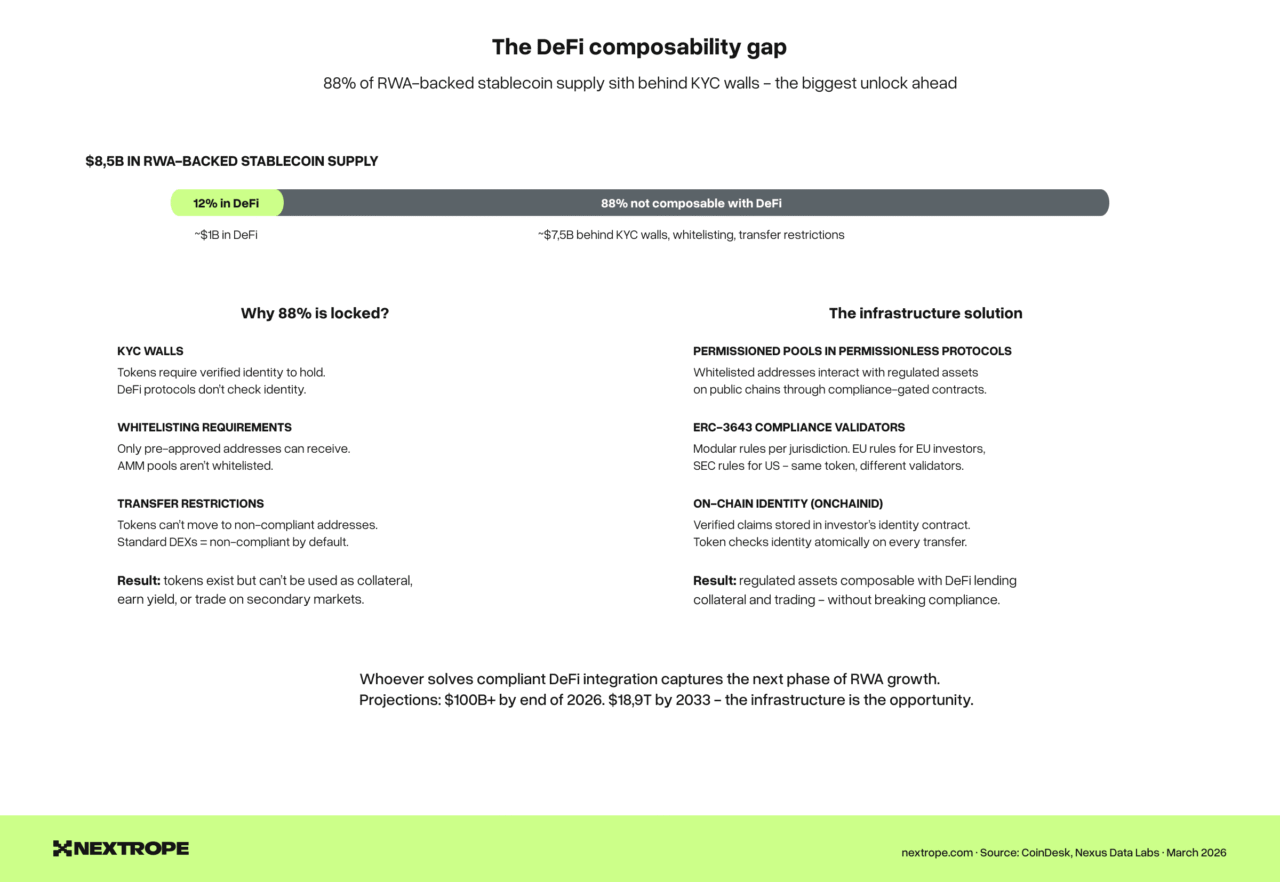

The DeFi composability gap

Here is the number that defines the next phase: only 12% of the roughly $8.5 billion in RWA-backed stablecoin supply is deployed in DeFi protocols. The remaining 88% sits behind KYC walls, whitelisting requirements, and transfer restrictions that prevent composability.

This is both the biggest problem and the biggest opportunity in RWA tokenization. The platforms that solve compliant DeFi integration – enabling tokenized assets to serve as collateral, earn yield, and trade on secondary markets while maintaining regulatory compliance – will capture the next wave of growth.

The technical pattern: permissioned pools within permissionless protocols. Whitelisted addresses interact with regulated assets on public chains through compliance-gated smart contracts. ERC-3643 was designed for exactly this use case – its modular compliance validators enable different rules for different jurisdictions, all enforced at the token level.

Build vs. integrate. The decision framework

Not every component needs to be built from scratch. The framework: build where you differentiate, integrate where commoditized.

Build in-house: Asset-specific business logic (your waterfall calculations, valuation methodology, compliance rules), user experience, and the integration layer that connects everything. This is your competitive advantage.

Integrate from vendors: KYC/KYB (Sumsub, Onfido), custody (Fireblocks, institutional custodians), oracle infrastructure (Chainlink), token standard frameworks (Tokeny for ERC-3643), and settlement rails.

Never build yourself: Custody infrastructure, unless you are a licensed custodian. The security requirements and regulatory expectations are too high for in-house development. A single compromised key can drain every token on the platform.

For teams evaluating the full spectrum of options, our build vs. buy analysis provides a detailed comparison across three approaches: fully custom, white-label, and modular assembly.

What this means for Your 2026 roadmap

The window for building RWA tokenization infrastructure is narrowing. MiCA’s full enforcement deadline is July 2026. Over 53 CASP licenses have been granted EU-wide. The institutions that are going to tokenize in this cycle are already selecting technology partners.

Three decisions determine your platform’s viability:

Token standard. ERC-3643 for multi-issuer, multi-jurisdictional platforms (most institutional use cases). ERC-1400 for single-jurisdiction, multi-tranche structured products. This decision is hard to reverse – choose based on your 24-month roadmap, not your launch requirements.

Compliance architecture. On-chain enforcement (ERC-3643) provides stronger MiCA compliance evidence. Off-chain enforcement (ERC-1400) gives more flexibility but requires separate audit infrastructure. The regulatory trend is toward provable enforcement – on-chain wins.

Build vs. integrate per subsystem. Build your asset logic and compliance rules. Integrate custody, KYC, and oracles. Don’t build custody. This allocation optimizes for both speed-to-market and competitive differentiation.

The $25 billion on-chain today is less than 0.01% of the addressable market. The infrastructure that captures the next 99.99% is being designed and built right now. The teams making the right architectural decisions today will operate the platforms that process trillions in tokenized assets by 2030.

Nextrope builds RWA tokenization infrastructure for financial institutions across Europe – from smart contract architecture and compliance middleware to yield distribution and regulatory reporting. Our engineering team has delivered turnkey solutions for Alior Bank and SOIL.

Let’s talk about your tokenization roadmap.