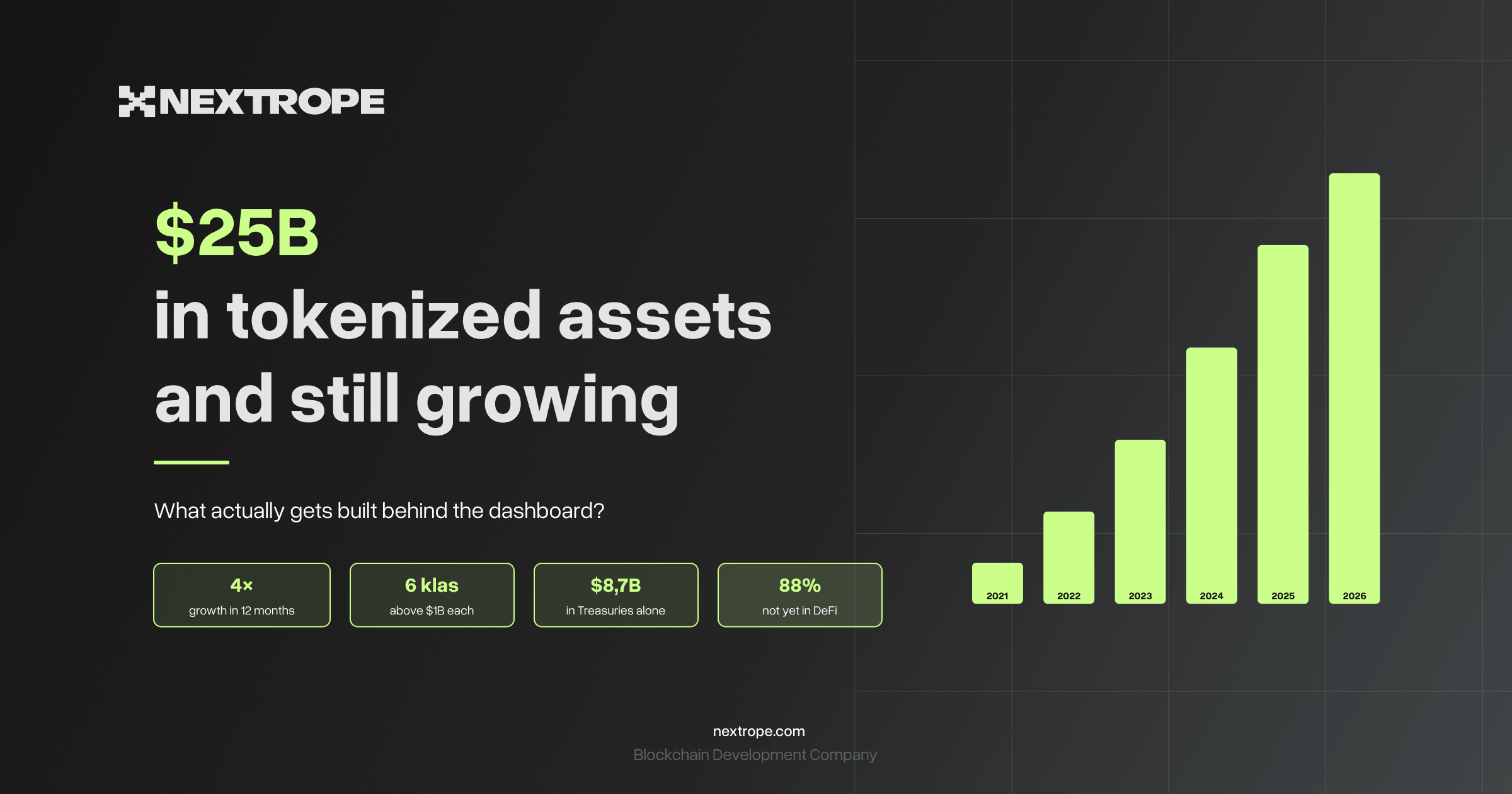

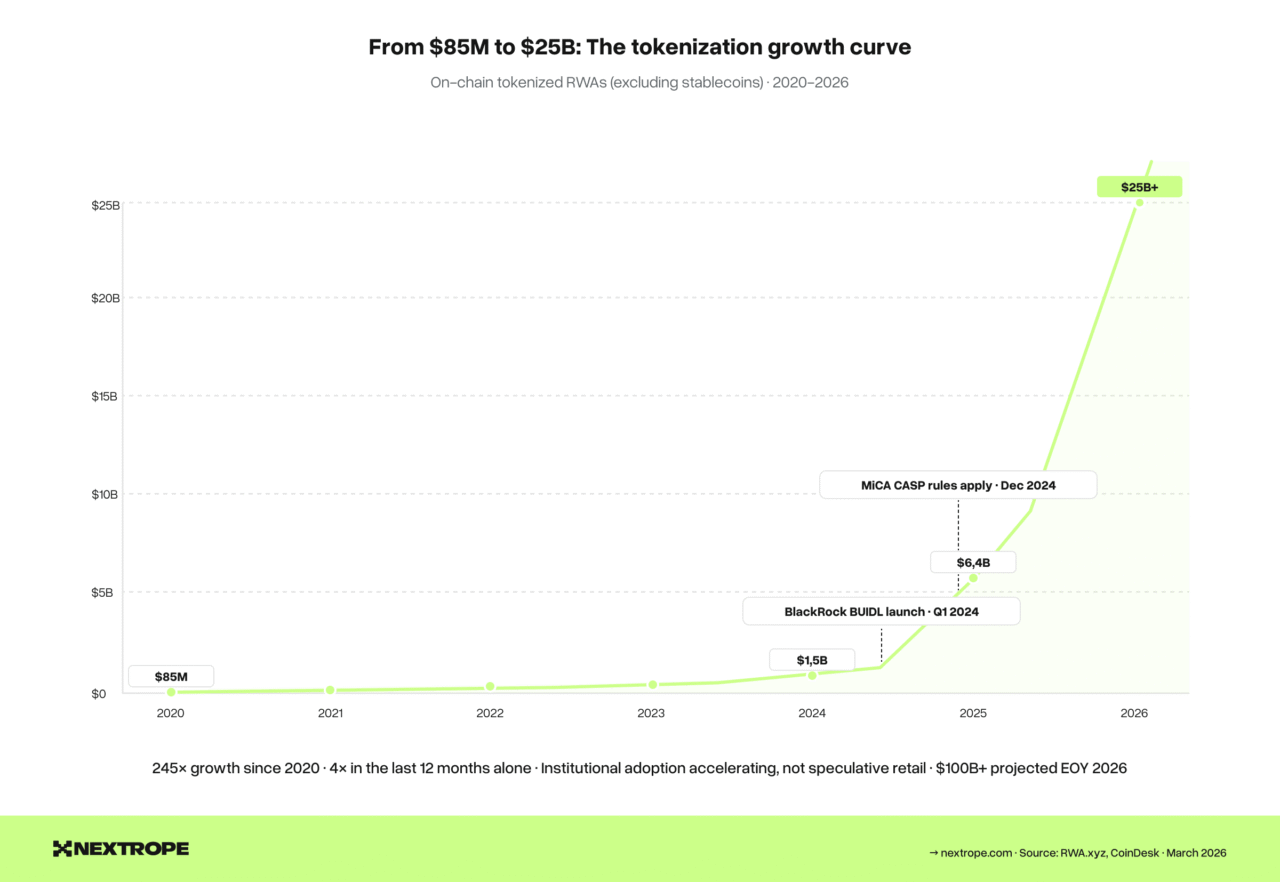

Tokenized real-world assets, excluding stablecoins, crossed $25 billion in on-chain value in March 2026, nearly quadrupling from roughly $6.4 billion a year earlier. Six distinct asset classes now each exceed $1 billion on-chain: US Treasuries, private credit, commodities, real estate, equities, and institutional funds.

These numbers get quoted in every industry report. What gets less attention is the engineering infrastructure behind them: the smart contracts, backend services, compliance middleware, and operational systems that make a tokenized asset actually function as a financial product. This article explores both sides: the market data that explains why institutions are tokenizing, and the technical architecture that determines whether their platforms work.

The Market: What changed in the last 12 months

Three structural shifts pushed tokenization from pilot phase to production infrastructure in 2025-2026.

Treasuries became the default on-chain yield product

Tokenized US Treasury and money-market fund assets reached $8.7 billion, growing 80% year-to-date. BlackRock’s BUIDL fund attracted over $550 million within months of launch. This is not speculative – it is institutions parking capital in the safest asset class available, using blockchain rails for operational efficiency rather than yield enhancement.

The engineering implication: Treasury tokenization requires real-time NAV calculation, daily dividend distribution logic, institutional-grade redemption flows with T+0 settlement, and tight integration with traditional custodians. The smart contracts are relatively simple; the backend integration with fund administrators, transfer agents, and banking rails is where the complexity lives.

Regulation created buying urgency

MiCA’s full enforcement deadline of July 2026 gave European institutions a concrete timeline. Over 53 CASP licenses have been granted EU-wide. The US GENIUS Act clarified stablecoin frameworks. SEC guidance in April 2025 confirmed that certain USD-backed stablecoins are not securities.

For platform builders, this means compliance is no longer a “nice to have” bolted on after launch — it is a prerequisite that shapes architecture from day one. Transfer restrictions, identity binding, Travel Rule compliance, and regulatory reporting must be baked into the smart contract and middleware layers. Our MiCA compliance checklist maps these requirements to specific engineering tasks.

The DeFi integration gap emerged

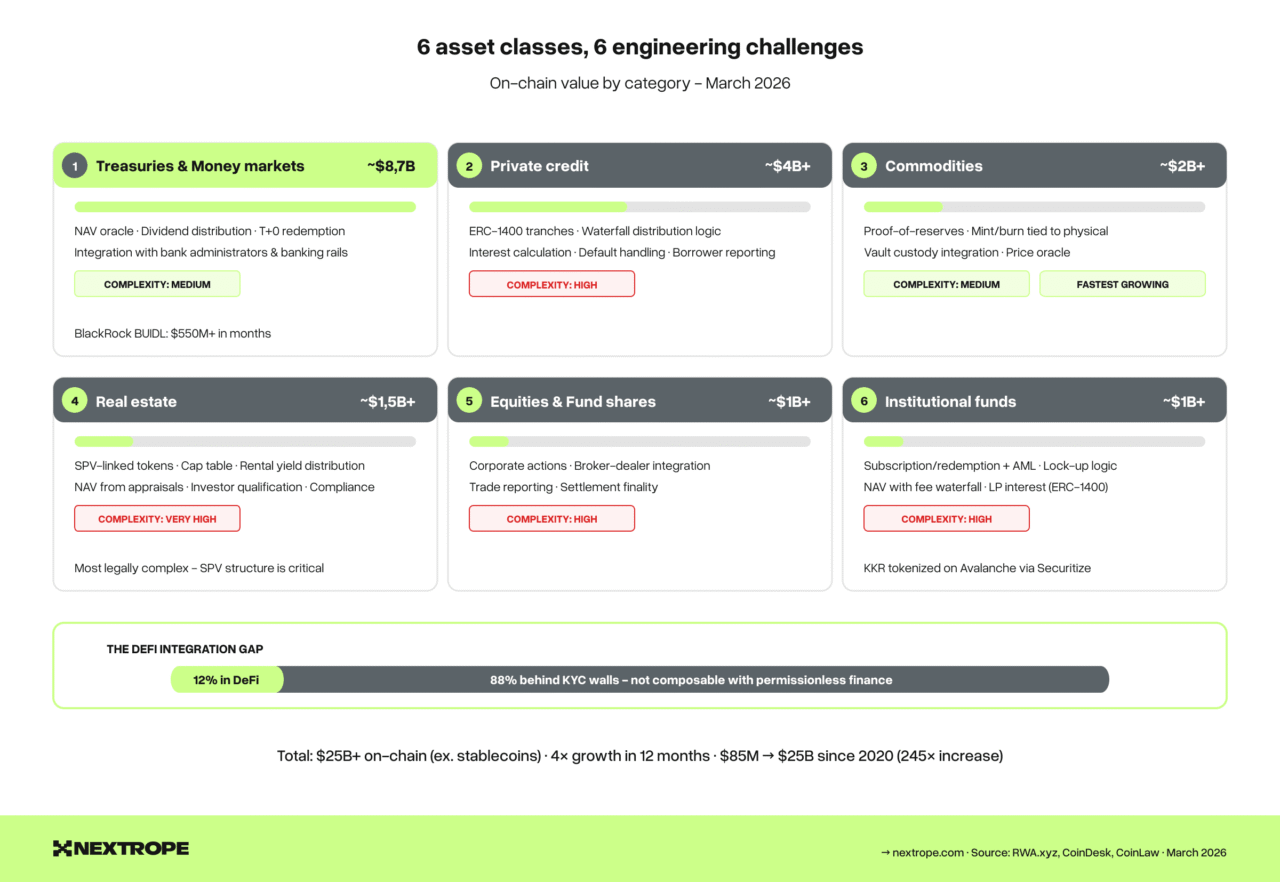

Here is the number nobody talks about: only 12% of the roughly $8.5 billion in RWA-backed stablecoin supply is actually deployed in DeFi protocols. The remaining 88% sits behind KYC walls, whitelisting requirements, and transfer restrictions that prevent composability with permissionless finance.

This is both a problem and an opportunity. The platforms that solve compliant DeFi integration – enabling tokenized assets to serve as collateral, earn yield, and trade on secondary markets while maintaining regulatory compliance – will capture the next phase of growth. The technical pattern that enables this is permissioned pools within permissionless protocols: whitelisted addresses interacting with regulated assets on public chains through compliance-gated smart contracts. Standards like ERC-3643 were designed precisely for this use case.

Six asset classes, six different engineering challenges

Each tokenized asset class carries distinct infrastructure requirements. A platform that tokenizes treasuries looks nothing like one that tokenizes real estate, even though both produce “tokens.”

1. Treasuries and money-market funds (~$8.7B)

The largest category and the simplest token logic. The underlying asset is a fund share; the token represents a claim on that share. Key engineering components: automated NAV oracle (daily price feed from fund administrator), dividend distribution contract (calculates and distributes yield per token), institutional redemption with T+0/T+1 settlement, and integration with authorized participant workflows for creation/redemption of fund units.

Complexity level: Medium. The smart contracts are straightforward, but the off-chain integration with traditional fund infrastructure is substantial.

2. Private credit (~$4B+)

Tokenized loans, receivables, and structured credit products. Unlike Treasuries, each position has unique risk characteristics — different borrowers, terms, collateral, and maturity dates. Key engineering components: tranche-based token architecture (ERC-1400 partitions work well here), waterfall distribution logic (senior vs. junior tranches), automated interest calculation and payment scheduling, default and liquidation handling, and borrower reporting integration.

Complexity level: High. The business logic is complex, with multiple token classes per deal and sophisticated payment waterfalls. See our architecture deep dive for how to structure multi-tranche systems.

3. Commodities (~$2B+, fastest growing)

Gold dominates, with Pax Gold (PAXG) and Tether Gold (XAUT) leading. Each token represents ownership of a specific quantity of physical gold held in vault custody. Key engineering components: proof-of-reserves system (linking on-chain supply to audited vault holdings), mint/burn mechanics tied to physical delivery, custody integration with vault operators, and real-time price oracle from commodity exchanges.

Complexity level: Medium. The token logic is simple, but the off-chain custody and audit integration is critical for credibility.

4. Real estate (~$1.5B+)

The most legally complex category. Tokenization does not change property law – it creates a digital representation of an interest in a legal structure (typically an SPV) that owns the property. Key engineering components: SPV-linked token with cap table management, rental yield distribution tied to property management systems, NAV updates from periodic appraisals, investor qualification checks (accreditation, jurisdiction), and compliance with real estate securities regulations.

Complexity level: Very High. Legal structuring, cross-jurisdictional compliance, and illiquidity management make this the most challenging asset class to tokenize properly. Teams that underestimate the legal wrapper complexity build platforms that cannot launch.

5. Equities and fund shares (~$1B+)

Tokenized stocks and fund interests, often through regulated intermediaries. Robinhood and Coinbase have begun offering tokenized private equities. Key engineering components: corporate action processing (dividends, splits, voting), broker-dealer integration, trade reporting to regulatory systems, and settlement finality mechanisms.

Complexity level: High. Heavily regulated, with extensive integration requirements with existing market infrastructure (CSDs, transfer agents, exchanges).

6. Institutional funds (~$1B+)

Tokenized LP interests, feeder fund units, and structured products. KKR tokenized a portion of its healthcare fund on Avalanche through Securitize. Key engineering components: subscription/redemption workflow with AML checks, investor eligibility verification (qualified purchaser, accredited investor), lock-up enforcement, and NAV calculation with management/performance fee waterfall.

Complexity level: High. Combines fund administration complexity with blockchain-specific engineering for token lifecycle management.

The infrastructure stack: What you actually build

Regardless of asset class, every tokenization platform shares a common architecture pattern. We break this down into six subsystems in our architecture deep dive, but here is the high-level view:

Smart contract layer – token standard selection (ERC-20+, ERC-1400, or ERC-3643), compliance hooks, upgradeability proxy, and transfer restriction logic. The standard choice depends on your asset class and compliance needs. Our ERC-3643 vs ERC-1400 comparison maps the decision framework.

Identity and Compliance middleware – KYC/KYB verification, on-chain claim registry, investor qualification engine, Travel Rule protocol integration, and transaction monitoring. This layer mediates between off-chain identity and on-chain token logic. Under MiCA, it is the orchestration point of the entire system.

Asset lifecycle engine – the off-chain backend that manages asset onboarding, valuation, document anchoring, and state transitions. Most teams underinvest here and pay for it later when they discover their data model cannot support the operations they need.

Distribution infrastructure – primary issuance pipeline (investor onboarding → subscription → payment reconciliation → minting) and secondary market integration (OTC, DEX, or order book). The bottleneck is almost always payment reconciliation — matching off-chain bank transfers to on-chain token allocations.

Custody and Key management – HSM/Cloud KMS for operational keys, MPC or multi-sig for high-value custody, and integration with institutional custodians. A single compromised key can drain every token on the platform.

Regulatory reporting – iXBRL white paper generation (mandated by ESMA since December 2025), order book record-keeping in ESMA JSON format, periodic disclosure automation, and audit trail management. This subsystem is often built last and asked about first by regulators.

The Build vs. Buy Decision

Not every component needs to be built from scratch. The decision framework: build where you differentiate, integrate where commoditized.

Build in-house: asset-specific business logic (your waterfall calculations, your valuation methodology, your compliance rules), user experience, and the integration layer that connects everything.

Integrate from vendors: KYC/KYB providers (Sumsub, Onfido), custody (Fireblocks, institutional custodians), oracle infrastructure (Chainlink), and potentially token standard frameworks (Tokeny for ERC-3643).

The one thing you should never build yourself: custody infrastructure, unless you are a licensed custodian. The security requirements and regulatory expectations are too high for in-house development.

For teams evaluating whether to build a custom platform or adopt a white-label solution, our build vs. buy analysis provides a detailed comparison of cost, time, and capability tradeoffs across three approaches.

What comes next

The $25 billion figure, impressive as it is, represents less than 0.01% of the total addressable market. Global fixed-income markets alone exceed $130 trillion. McKinsey projects $2 trillion in tokenized assets by 2030. Optimistic projections from industry leaders suggest $100 billion by the end of 2026.

The gap between current state and these projections will be filled by infrastructure – specifically, by platforms that solve three problems simultaneously: regulatory compliance across jurisdictions, composability with DeFi liquidity, and operational reliability at institutional scale.

The engineering teams that are building these platforms right now are making architectural decisions that will determine which asset classes they can support, which markets they can serve, and how quickly they can adapt as regulations evolve. Those decisions are not about choosing the trendiest blockchain or the most sophisticated consensus mechanism. They are about designing modular, compliant, production-grade systems that can operate under regulatory scrutiny while scaling to meet institutional demand.

The infrastructure buildout is the opportunity. The $25 billion is just the beginning.

Nextrope builds tokenization platform infrastructure for financial institutions across Europe. From smart contract architecture and compliance middleware to reserve management and regulatory reporting, our engineering team has delivered production platforms for clients including Alior Bank and SOIL. If you are evaluating tokenization infrastructure for your institution, let’s talk.