If you’re evaluating tokenization platforms right now, you already know the landscape has shifted. MiCA is live, the GENIUS Act is signed, and institutional demand for compliant token issuance has moved from “innovation lab” to “board agenda.” The question is no longer whether to tokenize but how to ship a platform that holds up in production.

This guide breaks down the real architecture decisions behind white-label tokenization, based on what we’ve learned building platforms for a European bank, multiple asset issuers, and regulated operators across three continents.

What “White-Label Tokenization” Actually Means in 2026

Two years ago, “white-label tokenization platform” mostly meant a cloned launchpad with your logo on it. The market has matured significantly since then.

Today, a production-grade white-label tokenization platform is an end-to-end issuance and lifecycle system: smart contracts, backend services, investor onboarding, compliance workflows, data indexing, and operational dashboards delivered under your brand, connected to your existing infrastructure.

The “white-label” part isn’t about slapping a logo on someone else’s SaaS. It’s about owning the platform while not rebuilding commodity infrastructure from scratch. You customize what differentiates you (asset model, compliance logic, investor experience) and leverage proven components for everything else (wallet integration, event indexing, deployment pipelines).

This distinction matters because the decision you’re actually making isn’t “build vs. buy.” It’s a three-way choice with very different trade-offs.

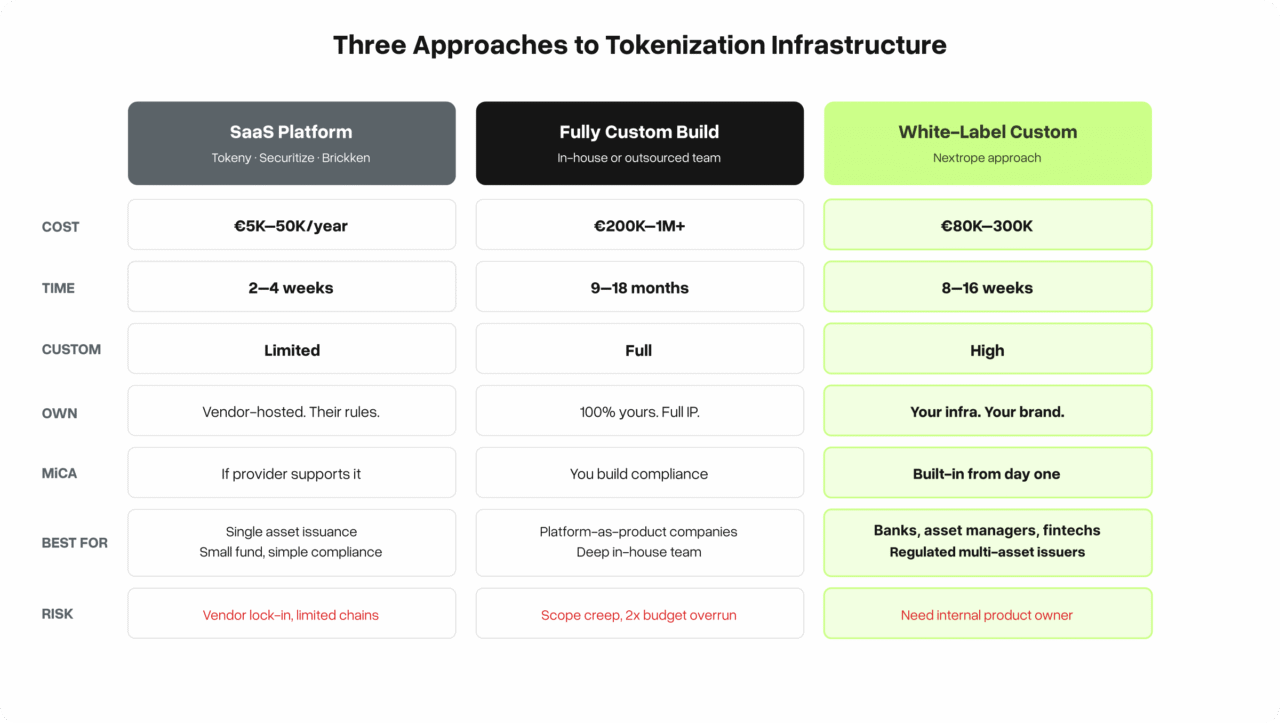

Three Approaches: SaaS, Custom Build, and White-Label Custom

Option 1: SaaS Platform (Tokeny, Securitize, Brickken)

You get a managed product. Token issuance, investor dashboard, basic compliance all hosted by the provider. You configure, don’t code.

Works when: You’re issuing a single asset or running a small fund and need to be live in weeks. Regulatory requirements are straightforward and the SaaS provider already supports your jurisdiction.

Breaks when: You need custom compliance logic (e.g., jurisdiction-specific transfer rules beyond standard whitelisting), integration with your existing core banking or CRM stack, or control over the data layer. You’re also locked into their token standard choices and chain support. If they don’t support XRPL or a specific L2 you’re out of luck.

Cost range: €5K–50K/year licensing + per-transaction fees.

Option 2: Fully Custom Build

You hire a blockchain engineering team (or build one) and construct everything from the ground up. Full control, full responsibility.

Works when: You’re building a platform that IS your core product (you’re essentially becoming a tokenization infrastructure provider yourself), you have deep in-house blockchain expertise, and your timeline is 9–18 months.

Breaks when: You underestimate the scope. A tokenization platform isn’t just smart contracts. It’s backend services for investor workflows, integration hooks for KYC/AML providers, indexers that turn blockchain events into operational data, deployment pipelines, monitoring, and incident response. Most teams that start “fully custom” end up rebuilding things that already exist and burning runway doing it.

Cost range: €200K–1M+ depending on scope and team location.

Option 3: White-Label Custom (What We Build at Nextrope)

You start from a proven architecture: contracts, backend patterns, integration templates and customize the layers that matter for your specific use case. The platform runs on your infrastructure, under your brand, with your compliance logic.

Works when: You need production-grade infrastructure but your differentiator is the asset model, the compliance framework, or the investor experience not the plumbing. You want to go live in 8–16 weeks instead of 12–18 months, without being locked into a SaaS vendor’s roadmap.

Breaks when: Your requirements are so unusual that no existing architecture applies (rare), or you’re looking for a quick demo and don’t care about production readiness.

Cost range: €80K–300K depending on complexity, integrations, and compliance scope.

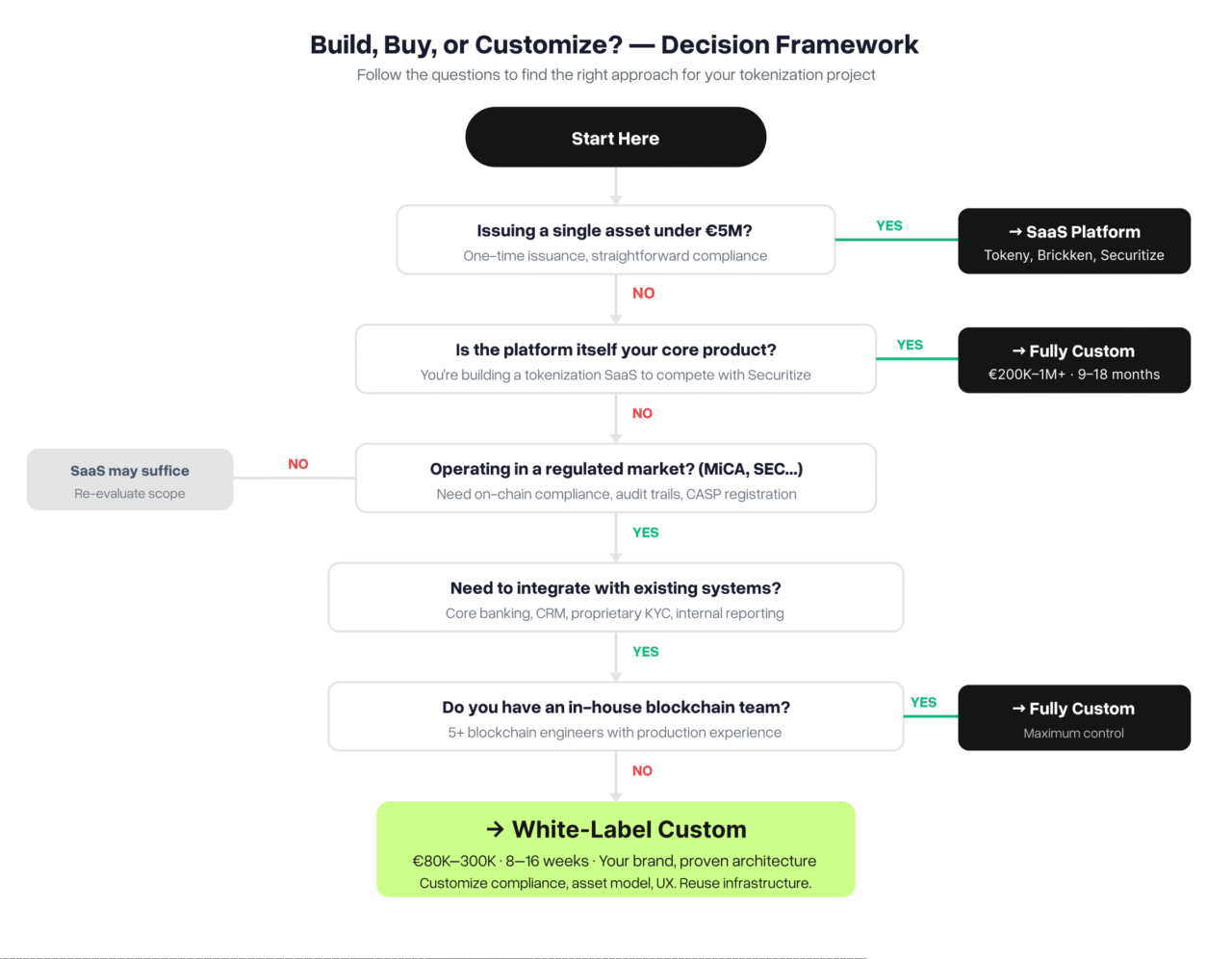

Which Approach Is Right for You?

Use this decision framework to narrow down your options based on your specific situation:

The flowchart above captures the critical questions we walk through with every client in the first discovery call. Most regulated issuers: banks, asset managers, fintechs adding digital assets to their stack land in the white-label custom zone. But there are legitimate cases for each approach, and we’ll tell you if SaaS or fully custom makes more sense for your situation.

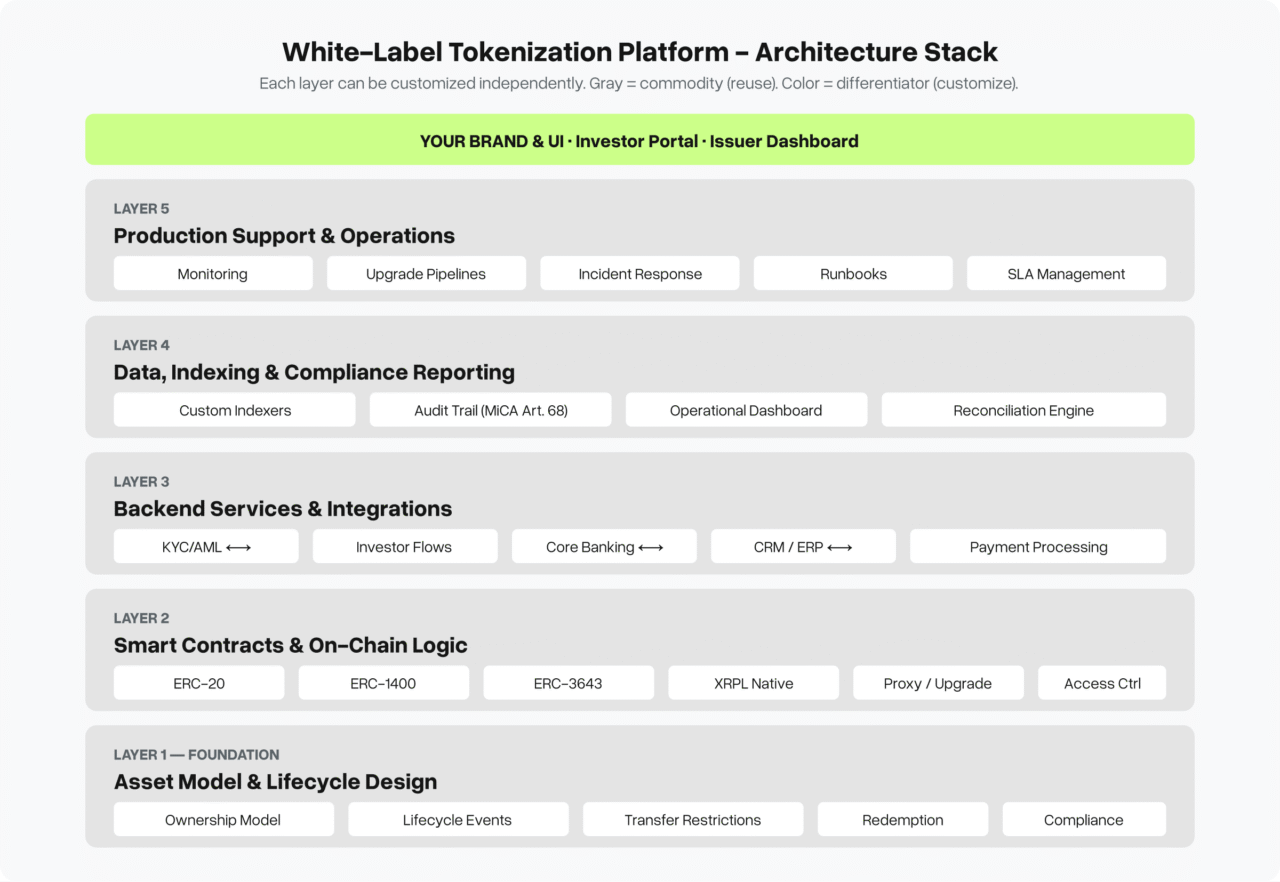

Architecture: What Actually Gets Built

Every tokenization platform we’ve shipped from Alior Bank’s document integrity system to commodity-backed issuance for a Canadian operator follows a similar layered architecture. The layers differ in complexity depending on the use case, but the structure is consistent.

Layer 1: Asset Model and Lifecycle Design

Before any code gets written, you need a clear specification of what the token represents, how it’s issued, transferred, redeemed, and what lifecycle events it goes through.

This is where most projects get it wrong. They jump to “which token standard should we use?” before answering fundamental questions:

- Ownership model: Does the token represent fractional equity? A debt instrument? A claim on a physical commodity? Each has different transfer semantics.

- Lifecycle events: What happens at maturity? How are dividends or yield distributed? Can tokens be force-transferred for compliance? Can they be frozen?

- Transfer restrictions: Which investors can hold this token? Is it jurisdiction-specific? Does it require ongoing KYC verification?

- Redemption: Can holders redeem for the underlying asset? Under what conditions? What’s the settlement flow?

The output of this phase is a specification that maps business rules to on-chain and backend components. This document drives everything downstream.

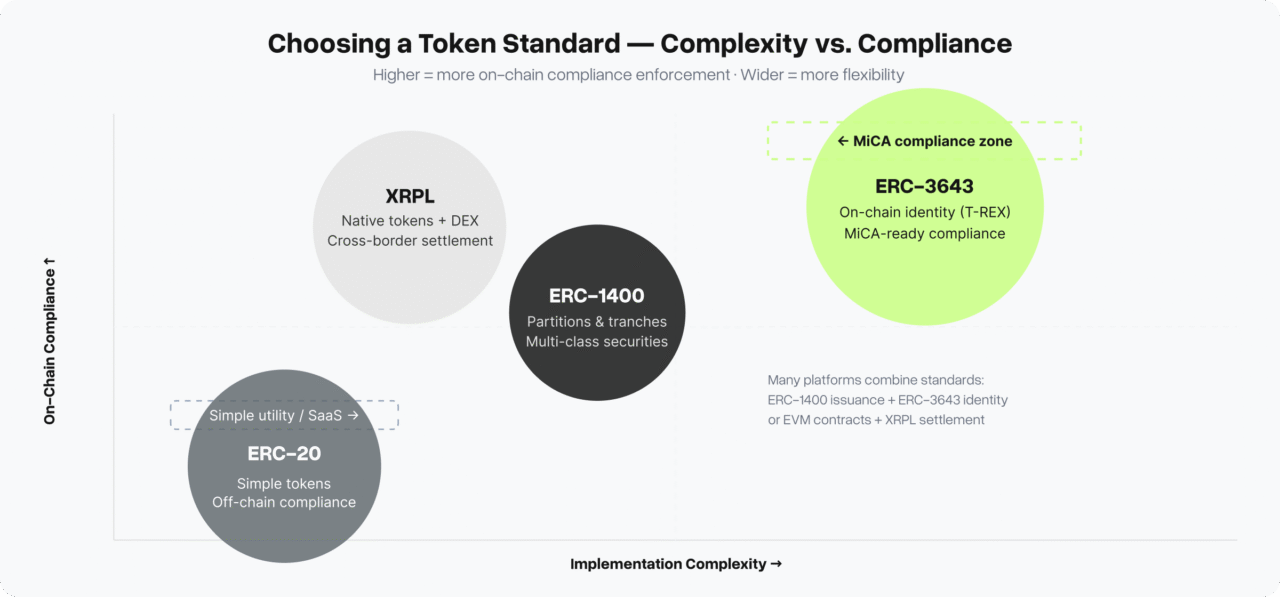

Layer 2: Smart Contracts

The choice of token standard is an engineering decision driven by your asset model, not a marketing decision.

ERC-20 works for simple utility tokens or representations where you handle compliance entirely off-chain. Minimal on-chain logic, maximum flexibility in your backend.

ERC-1400 (Security Token Standard) adds partitions – the ability to group tokens by tranche, class, or issuance date. This matters for structured products, multi-class equity, or instruments where different holders have different rights. Each partition can have its own transfer rules. If your asset model requires distinguishing between Series A tokens and Series B tokens within the same contract, ERC-1400 is the standard to use.

ERC-3643 (T-REX) builds compliance directly into the token. Identity verification, transfer eligibility, and claim validation happen on-chain through a modular identity framework. A transfer won’t execute unless the recipient has the required verified claims (e.g., accredited investor status in the right jurisdiction). This is the standard most aligned with MiCA’s requirements for on-chain compliance enforcement.

XRPL native tokens offer a different model entirely – tokens issued directly on the XRP Ledger with built-in DEX functionality, trust lines, and clawback capabilities. For issuers targeting the Ripple ecosystem or needing cross-border settlement via XRPL’s native capabilities, this is increasingly relevant. We’ve built XRPL tokenization flows for SOIL’s cross-chain implementation and it’s a fundamentally different architecture than EVM-based approaches.

In practice, the choice often isn’t either/or. We’ve shipped platforms that use ERC-1400 for the primary issuance with ERC-3643-style identity checks layered on top, or hybrid architectures with EVM contracts for the core token and XRPL flows for settlement.

Layer 3: Backend Services and Integrations

This is the layer that SaaS platforms handle for you and the layer that breaks first when you outgrow them.

Issuer workflows: Admin panels for managing issuance rounds, approving transfers, triggering lifecycle events (dividends, maturity, forced transfers). Connected to your internal approval processes.

Investor onboarding: Integration with your chosen KYC/AML provider (Sumsub, Onfido, Veriff, or your bank’s existing identity system). Whitelist management that syncs with on-chain permissions.

Payment rails: Fiat on/off ramps (bank transfer, card payments) connected to your treasury. Increasingly, stablecoin settlement (USDC, RLUSD) as an alternative which requires its own compliance framework under MiCA’s EMT rules.

Cap table and registry: The authoritative record of who owns what. This must reconcile with the on-chain state but also needs to handle edge cases the blockchain doesn’t know about (legal disputes, inheritance, corporate actions).

Layer 4: Indexing, Reporting, and Data Integrity

The most underestimated layer. Your finance team, compliance team, and operations team don’t read blockchain explorers. They need:

- Real-time event indexing that turns on-chain events (transfers, issuance, redemptions) into database records your backend can query.

- Operational dashboards showing AUM, investor distribution, transaction volumes, compliance status.

- Audit-ready reporting – transaction logs with timestamps, actor identification, and compliance check results. This is explicitly required under MiCA Article 68 for crypto-asset service providers.

- Reconciliation tools that flag discrepancies between on-chain state and your backend records.

We build custom indexers for every platform because generic solutions (The Graph, Moralis) don’t cover the compliance metadata most regulated issuers need.

Layer 5: Launch Readiness and Production Support

Going live isn’t the end. It’s the beginning of operational responsibility.

- Monitoring and alerting for contract interactions, gas costs, indexer lag, and integration health.

- Runbooks for common operational scenarios: investor can’t access wallet, transaction stuck, compliance check failure.

- Safe upgrade paths for smart contracts (proxy patterns, timelock governance) that don’t require migrating investor positions.

- Incident response basics – who gets paged, what gets rolled back, how you communicate with investors.

MiCA Changes Everything for European Issuers

If you’re building a tokenization platform for the European market in 2026, MiCA (Markets in Crypto-Assets Regulation) isn’t optional, it’s the architecture driver.

Key requirements that directly impact platform design:

Whitepaper obligations (Title II): Every crypto-asset offered to the public needs a published, standardized whitepaper. Your platform needs a whitepaper management workflow – drafting, review, publication, and versioning – built into the issuer dashboard.

CASP registration (Title V): If your platform facilitates trading or custody, you need CASP (Crypto-Asset Service Provider) authorization. The technical requirements include cybersecurity frameworks, business continuity, and audit trails that your platform must generate.

Transfer restriction enforcement: MiCA expects issuers to demonstrate that transfer restrictions are actually enforced, not just promised. On-chain compliance (ERC-3643 style) is stronger evidence than backend-only checks.

Record-keeping (Article 68): Five years of transaction records with full traceability. Your data layer needs to be designed for long-term, audit-grade storage from day one.

EMT rules for stablecoin settlement: If your platform supports stablecoin payments (increasingly demanded by institutional investors), the stablecoin itself must comply with MiCA’s Electronic Money Token requirements. This affects which stablecoins you can integrate and how.

Most white-label providers outside Europe haven’t internalized these requirements yet. Their platforms were designed for pre-MiCA markets. Retrofitting compliance is significantly harder and riskier than building it in from the start.

What We’ve Learned From Shipping Real Platforms

Some lessons from platforms we’ve built that you won’t find in generic “top 10 tokenization platforms” listicles:

The asset model phase saves more money than any other. We spent three weeks on asset modeling for a New Zealand real estate tokenization project. That upfront investment meant zero rework during smart contract development. Compare that with projects we’ve seen (not ours) where teams coded contracts first and redesigned the asset model twice burning 4–6 months.

On-chain compliance is worth the complexity. Early tokenization platforms handled compliance entirely in the backend – whitelist checks before submitting transactions. This works until an investor’s status changes between the check and the transaction, or until a regulator asks you to prove enforcement. On-chain compliance (verified claims, transfer restrictions in the contract) is harder to build but dramatically easier to audit and defend.

Multi-chain isn’t a feature – it’s an architecture decision. “We support Ethereum, Polygon, BSC, and Solana” sounds impressive on a landing page. In practice, each chain has different finality guarantees, gas models, and tooling. A platform that genuinely supports multiple chains needs chain-specific indexers, different deployment pipelines, and a backend that abstracts chain differences without hiding them. We typically recommend picking one primary chain and adding others only when there’s a concrete business case.

Investor onboarding is 40% of the work. The sexy part of tokenization is the smart contract. The hard part is making it usable for real investors – identity verification, wallet provisioning (or custodial wallet integration), payment processing, and clear communication at every step. Platforms that nail the contract but fumble onboarding don’t get used.

How to Evaluate a White-Label Tokenization Partner

If you’re shortlisting providers, here’s what to ask:

- “Show me a platform you’ve shipped that’s in production.” Not a demo. Not a testnet deployment. A real platform with real investors and real assets. If they can’t show you one, they’re selling templates, not infrastructure.

- “Which token standards do you support, and why would I choose one over another?” If the answer is “we use ERC-20 for everything” or “we support all standards” without nuance, they haven’t built for regulated issuers.

- “How do you handle compliance under MiCA / GENIUS Act / [your jurisdiction]?” If they haven’t heard of MiCA or can’t explain the specific technical requirements, they’re not building for the 2026 market.

- “What does production support look like after launch?” If they hand you the code and disappear, you’ll be on your own when something breaks at 2 AM on a Sunday.

- “Can you integrate with my existing systems?” KYC provider, banking core, CRM, reporting tools. If the platform is a closed box that requires you to adapt to it (rather than the other way around), you’ll spend more on integration than on the platform itself.

When White-Label Isn’t the Right Answer

To be transparent: white-label tokenization isn’t always the right choice.

If you’re issuing a single asset under €5M – a SaaS platform like Tokeny or Brickken will get you live faster and cheaper. The overhead of a custom platform isn’t justified.

If tokenization is your entire business and you’re building a platform to compete with Securitize or Tokeny you should build fully custom. Your platform IS your competitive advantage, and you shouldn’t share architecture DNA with competitors.

If you don’t have internal technical capacity to operate the platform even a white-label platform needs someone who understands it. We provide production support, but you still need an internal team member who owns the platform as a product.

For everything in between: regulated issuers, asset managers tokenizing multiple products, banks adding digital asset capabilities, fintechs building tokenization into their stack – white-label custom is typically the right combination of speed, control, and cost.

FAQ

How much does a white-label tokenization platform cost? For a production-grade platform with compliance workflows, custom integrations, and multi-standard smart contracts: €80K–300K. Simple MVPs start lower; complex multi-jurisdiction platforms with core banking integration can go higher. We scope every project individually.

How long does it take to build? Typical timeline from discovery to production: 8–16 weeks. This assumes clear asset model requirements and KYC/AML provider selection upfront. Platforms requiring novel compliance frameworks or unusual blockchain integrations take longer.

Which blockchain should I use for tokenization? It depends on your asset model and investor base. Ethereum (or an L2 like Polygon/Base) is the default for EVM-compatible security tokens. XRPL is compelling for cross-border settlement and issuers in the Ripple ecosystem. We’ve built on both and often recommend starting with one chain, then expanding.

Do I need ERC-3643 for MiCA compliance? Not strictly required, but it’s the strongest technical evidence of on-chain compliance enforcement. ERC-1400 with backend compliance checks can also work, but you’ll need to document your enforcement mechanisms more thoroughly for regulators.

Can I migrate from a SaaS platform to white-label later? Yes, but it’s not painless. Token holder positions need to be migrated (or bridged), investor data must be re-onboarded, and integrations rebuilt. It’s cheaper to start with the right architecture than to migrate. We’ve helped clients transition from SaaS to custom. The typical timeline is 12–20 weeks including migration.

Next Steps

We build tokenization platforms for institutional issuers, asset managers, and fintechs typically from discovery to production in 8–16 weeks.

If you’re evaluating your options:

→ See our tokenization case studies – Alior Bank, SOIL, commodity tokenization, real estate tokenization, and more.

→ Book a 30-minute architecture call – We’ll map your asset model and give you an honest assessment of whether white-label custom makes sense for your use case.

→ Read: ERC-3643 vs ERC-1400 – Choosing a Token Standard After MiCA – Deep technical comparison of the two leading security token standards.

Related articles in this cluster:

- MiCA Phase 2: Technical Checklist for Tokenization Platforms in Europe (coming soon)

- Tokenization Platform Architecture: What Actually Gets Built (coming soon)