The GENIUS Act entered into force on July 18, 2025, while MiCA requires stablecoin issuers to obtain authorization by July 1, 2026. Those who fail to do so will lose access to the EU market. Twelve European banks, including BBVA, have formed the QiValis consortium to jointly launch a regulated euro-pegged stablecoin in the second half of this year.

These systems are now being planned, budgeted, and built, and the following article provides a technical perspective. Without delving into regulatory theory, we discuss what systems and integrations need to be implemented for stablecoins to actually function in production.

The regulatory landscape in 60 seconds

Two frameworks now define the global stablecoin market:

US GENIUS Act – federal law since July 2025. Payment stablecoins must be backed 1:1 by USD, treasuries, or insured deposits. Monthly reserve reports with criminal penalties for false certification. No interest or yield payments. Issuers above $10B fall under Federal Reserve or OCC supervision. Final rules targeted July 2026.

EU MiCA – two token categories. E-Money Tokens (EMTs) reference a single fiat currency. Asset-referenced tokens (ARTs) reference baskets. EMT issuance requires EMI authorization – a banking-adjacent license. Hard deadline: July 1, 2026. Non-authorized issuers face delisting.

The engineering insight: both frameworks converge on the same core – licensed issuance, 1:1 reserves, segregated custody, instant redemption, full AML/KYC. The architecture pattern is the same even though the specific implementations differ.

For institutions targeting both markets, the reserve architecture must satisfy both simultaneously. Designing for one and retrofitting for the other is significantly more expensive than getting it right from the start.

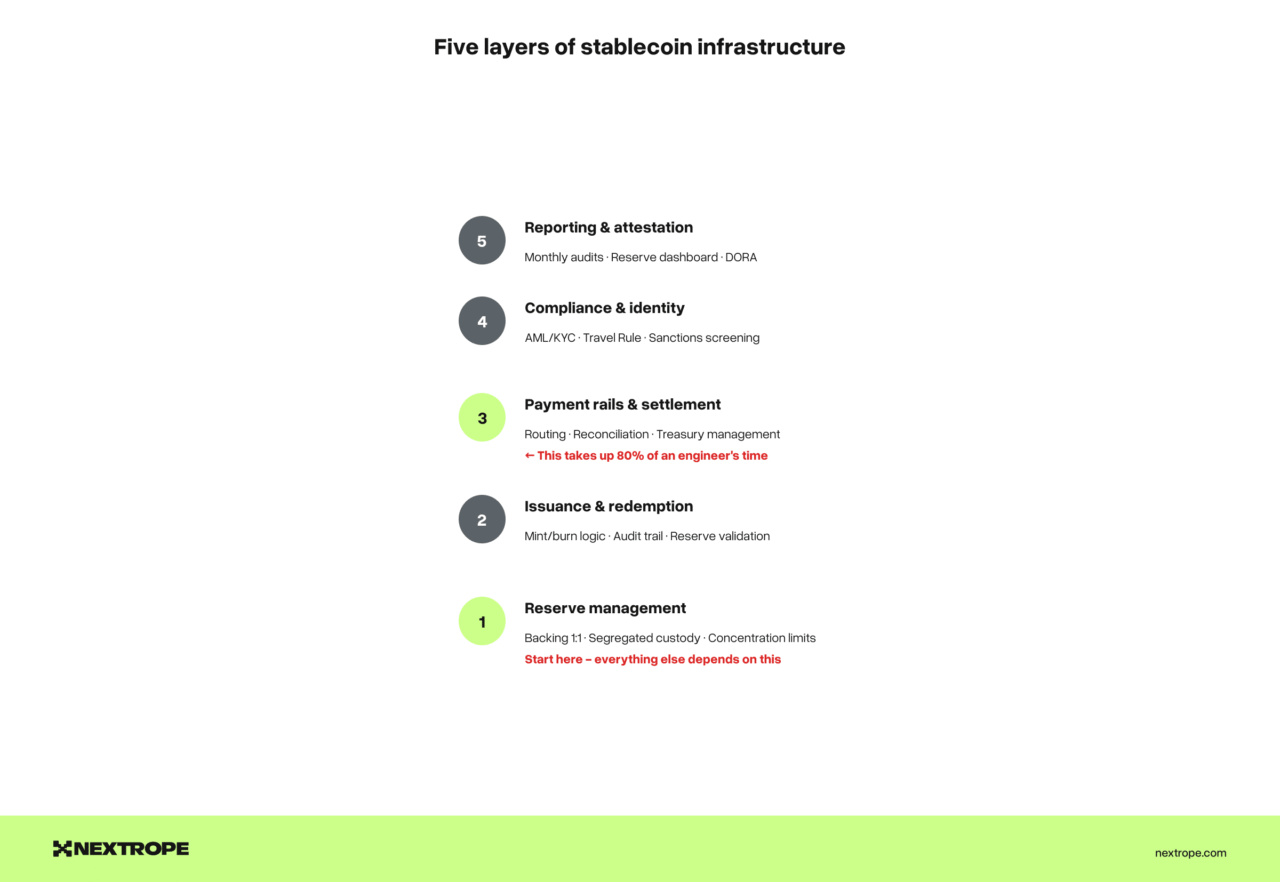

The five infrastructure layers

Every stablecoin operation, whether issuing your own token or building payment infrastructure around USDC or RLUSD, requires five layers.

Layer 1: Reserve management

The foundation. Under both frameworks, reserves must be in high-quality liquid assets, segregated, and independently audited.

What you build: real-time reserve tracking, concentration limit enforcement (MiCA requires 60% of EMT reserves in EU credit institutions), rebalancing triggers, and monthly attestation report generation.

The non-obvious challenge: reserve accounts satisfying GENIUS Act but held with custodians not authorized under MiCA will need restructuring for EU authorization. Fixing this after launch is significantly more expensive.

Layer 2: Issuance and redemption

The core product logic. Minting and burning must be atomic, auditable, and compliant.

What you build: an issuance engine that validates every mint against reserve availability, processes redemptions within guaranteed timeframes (MiCA: par value at any time), and maintains a complete audit trail linking every token to its reserve backing.

The smart contract is the simplest part, since it’s an ERC-20 with mint/burn restricted to authorized addresses. The complexity lives in off-chain orchestration, ensuring the reserve deposit is confirmed before mint executes, and burn is confirmed before fiat transfer initiates.

Layer 3: Payment rails and settlement

Where stablecoins deliver actual business value. Settlement connects on-chain movement to off-chain banking infrastructure.

What you build: payment routing (stablecoin-to-stablecoin, stablecoin-to-fiat, fiat-to-stablecoin), settlement reconciliation matching on-chain transactions to bank ledger entries, and treasury management for float and liquidity.

The bottleneck: payment reconciliation. The bank wire says “REF: PAY-4821.” The blockchain says “0x7a3b…sent 250,000 USDC to 0x9f2c.” Matching these reliably at scale consumes the most engineering time. The same bottleneck we see in tokenization platforms – check out our architecture deep dive.

For XRPL-based flows (RLUSD), the architecture differs. XRPL’s built-in DEX and payment path-finding simplify multi-hop settlement. Our team built these flows for SOIL.co’s stablecoin operations.

Layer 4: Compliance and identity

Full AML/KYC, Travel Rule, transaction monitoring, and sanctions screening.

What you build: identity verification for every participant in stablecoin flows. Real-time transaction monitoring. Travel Rule implementation (€1,000 under MiCA, $3,000 under GENIUS Act). Sanctions screening on every transaction.

The architectural decision: on-chain compliance (ERC-3643 style) vs. off-chain middleware. For high-volume payment flows, off-chain compliance with on-chain audit anchoring is typically more practical. Volume and speed favor backend processing with blockchain as the settlement and audit layer.

Layer 5: Reporting and attestation

Built last, asked about first.

What you build: monthly reserve attestation reports (audited by registered firms), real-time reserve dashboards, regulatory flow reporting, AML/SAR integration, and tax reporting under CARF (EU).

The DORA requirement (EU): stablecoin issuers must comply with the Digital Operational Resilience Act, including ICT risk management, incident reporting, and resilience testing. Adds 2-3 months to implementation timelines.

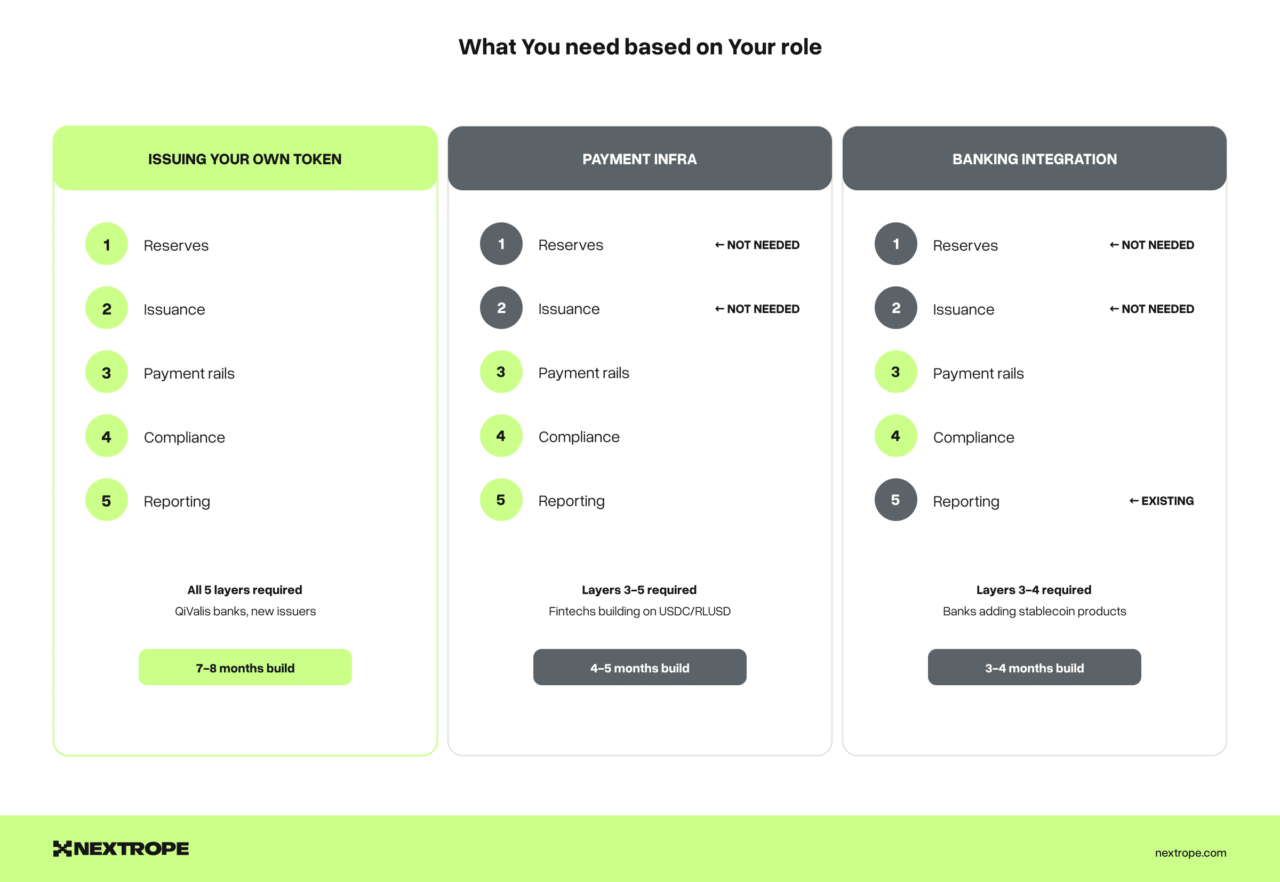

Build vs. partner

Issuing your own stablecoin: You need all five layers. Reserve management and issuance are your core competency.

Building payment infrastructure around USDC/RLUSD: You need layers 3-5. You’re routing and settling, not minting.

Integrating stablecoins into existing banking products: Primarily layers 3 (payment rails) and 4 (compliance), integrated with core banking.

The timeline

MiCA: July 1, 2026.

GENIUS Act final rules: July 2026.

Hong Kong first licenses: H1 2026.

Realistic build timeline for a focused team with stablecoin experience is 7-8 months from architecture to launch. Teams without prior regulated financial infrastructure experience add 2-3 months.

What comes next

The stablecoin market exceeded $310 billion in early 2026. USDC volume in Europe jumped 337% after Circle achieved MiCA compliance. Fourteen issuers now hold MiCA authorization across seven EU member states. The QiValis consortium of 12 European banks is launching a regulated euro stablecoin.

The institutions building stablecoin infrastructure now will operate the payment rails that process trillions by 2030. The window is narrow. Authorization backlogs are growing and first-mover advantage is real.

Nextrope builds stablecoin infrastructure for financial institutions across Europe. Our team has delivered production platforms for clients, including Alior Bank and SOIL. From reserve management and issuance engines to payment rail integration and compliance middleware.

Let’s talk about your stablecoin roadmap.